During February 2025, Europe saw a decline in power purchase agreement (PPA) prices. According to Pexapark’s monthly report, the EURO Composite Index closed at €50.25/MWh, down 4.3% compared to January. This drop aligned with the general fall in energy commodity prices, also driven by mild temperatures and bearish gas market trends throughout the month.

The Nordic market was the only region to experience a price increase in February, with a modest month-on-month rise of 0.6%. This came after a sharp drop in January due to strong hydrological conditions and mild weather. Prices recovered slightly at the end of February, supported by drier outlooks.

Portugal recorded the largest monthly decline at 10.9%, following a recalibration of reference prices for pay-as-produced solar PV PPAs. Italy (-6.6%), France (-5.3%), and Germany (-4.4%) followed, reflecting continued downward pressure from electricity and gas markets.

Meanwhile, the United Kingdom saw a 3.5% drop, followed by the Netherlands (-3.3%) and Spain (-3.2%).

It’s worth noting that Spain’s solar PPA market is currently facing one of its most challenging periods. Miguel Marroquín, Managing Director at Our New Energy, explains that buyers are bidding for solar energy at between €25 and €30/MWh, but emphasizes: “For a producer to sign a PPA that makes sense, the contract needs to be at least €35.”

In this context, the few PPAs being signed are at the upper end of that range—€30/MWh—and only for projects with extremely competitive conditions.

Stable volumes, shifting signals

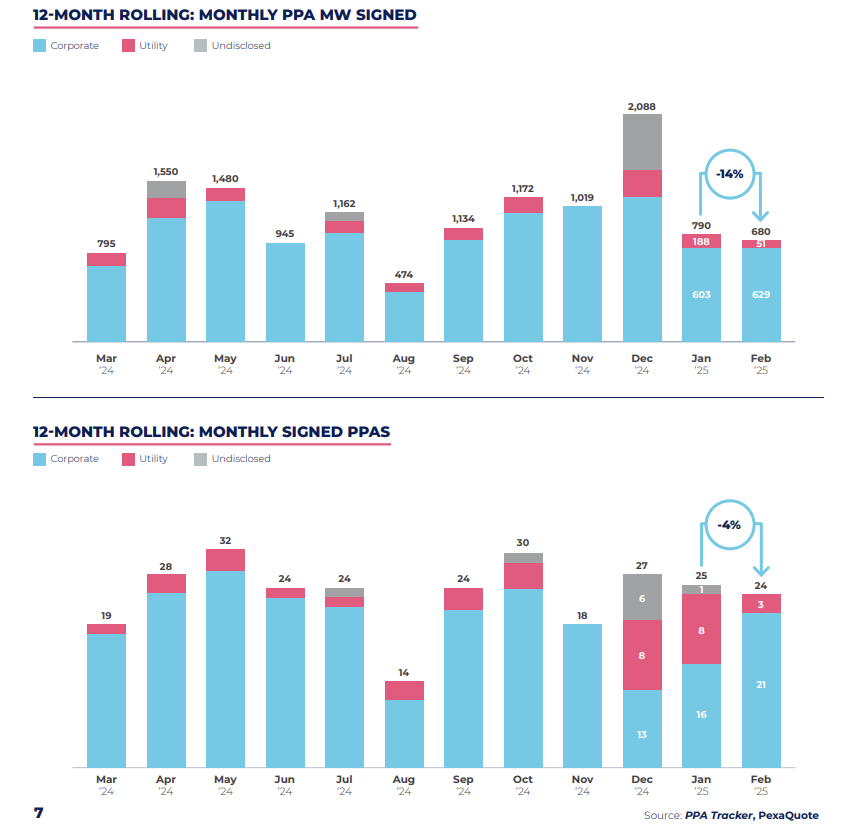

Beyond prices, deal flow showed signs of cooling. In February, 24 PPAs were announced totaling 679.8 MW, representing a 14% decline in volume and a 4% decrease in the number of deals compared to January.

However, this monthly slowdown must be seen in a broader context: Europe signed a record-breaking 15.2 GW in PPAs during 2024. Activity remains high, although deals are increasingly spread out and smaller in volume.

Compared to last year, monthly figures look quite different. February 2024 was a record month with 54 PPA announcements, meaning a year-on-year drop of more than 55%. In terms of capacity, 2,568 MW were announced in February 2024, compared to 679.8 MW in February 2025—a 73.5% decrease.

Among February’s most notable deals was a 130 MW virtual PPA between X-Elio and the Energize Program, which includes pharma companies like GSK and Thermo Fisher. Another key deal was a 98 MW multi-country PPA between BNZ and Kimberly-Clark, expected to generate 164 GWh annually from two solar plants in Italy and one in Spain.

Rounding out the top three was a 57 MW PPA between Zelestra and Tesla, linked to three solar projects in Brazatortas, Castilla-La Mancha, with construction starting soon. Other major players like ERG and Amazon also signed PPAs.

A new duration record in Wales

A milestone of the month came with the announcement of a 40-year physical solar PPA between Innova and Dŵr Cymru (Welsh Water)—the longest PPA ever recorded in Europe, covering 15 MW of capacity. The agreement will source energy from the Wrexham and Cefn solar farms, located in southern and western parts of the Wrexham Industrial Estate in Wales.

“In Europe, long-term PPAs have typically ranged from 5 to 25 years, with the previous record at 30 years. This Welsh PPA is the first publicly announced 40-year contract, setting a new benchmark,” Pexapark notes.

They also highlight that longer-term PPAs—typically 20 to 30 years—often share common features: solar PV technology, physical on-site structures, and pay-as-produced (PAP) volume structures.

In Great Britain, 26 PPAs were announced in 2024 totaling 1,032 MW, with corporate buyers representing 92% of deals. This trend continues in 2025, with all three PPAs announced so far being corporate-driven.

Momentum for multi-buyer PPAs

Multi-buyer PPAs are gaining ground as an innovative structure across Europe. February saw the first such agreements of 2025, including one between X-Elio and the Energize Program, where four companies will offtake 245 GWh annually—35% of the 369 MW Lorca Solar project in Murcia, Spain. The project is expected to be operational by early 2026.

This marks the third multi-buyer PPA in Spain enabled by the Energize Program, which facilitated over 280 MW of new solar capacity in 2024 through deals with Zelestra and Bruc Energy.

Meanwhile, in Denmark, Norlys and Eurowind Energy signed a PPA with DS Gruppen A/S and Arbejdernes Landsbank for a 124.5 MW solar-wind hybrid portfolio expected to generate 252 GWh annually. The two buyers will offtake around 20% of the portfolio’s output (estimated PPA size: 24.9 MW), with the agreement coming into effect in 2027.

“It’s only February, but the momentum behind multi-buyer PPAs in Europe is already evident. We expect this trend to continue growing,” the report underlines.

To date, 21 such deals have been publicly announced across Europe since 2016, with Spain (6) and Denmark (7) leading the way.

Regulatory push in Italy

February also marked a major regulatory milestone in Italy with the Transitional FER X Decree coming into force. Valid through December 2025, it provides differentiated incentives by technology:

-

10 GW for solar PV

-

4 GW for wind

-

0.63 GW for hydro

-

0.02 GW for biogas

Projects under 1 MW can directly access incentives, while larger projects must participate in competitive auctions.

Surge in tolling and co-location in energy storage

Another emerging theme from the report is the rising interest in tolling agreements in the battery storage sector. These arrangements allow utilities, traders, or industrials to lease battery capacity through fixed payments, shifting market risk to the offtaker.

“The cost of capital is the biggest barrier in the energy transition, and tolling agreements are key tools to unlock cheaper financing,” Pexapark explains.

Meanwhile, solar-plus-storage co-location is also gaining traction, especially under AC-coupled setups. Though valuation tools are still evolving, co-location is seen as a cost-effective way to optimize grid connections and enable independent business models.

Switzerland begins to emerge

Although lagging behind other European markets, Switzerland is beginning to show signs of PPA activity. In February, Swiss Federal Railways (SBB) signed a 20-year PPA with Axpo for solar power from the 8 MW NalpSolar project in the Alps.

Despite a slower market, interest in PPAs is growing. A recent example from 2024 is Romande Energie’s agrivoltaic PPA with supermarket chain Denner, located in Conthey, Valais. It is expected to start operations mid-2025 and produce around 600 MWh annually.

In January 2025, Alpiq also signed a 10-year PPA with Stadtwerke Wetzikon to supply power from its Flumenthal and Gösgen hydropower plants on the Aare river.