The year 2025 is shaping up to be a decisive moment for the development of offshore wind energy in Spain. Despite being one of the countries with the greatest potential to become a leader in floating offshore wind energy, the sector faces crucial challenges due to the lack of regulatory definitions and the postponement of the necessary public auctions to finance and execute the first commercial projects.

The publication of the Royal Decree in 2024 marked a significant step forward by establishing the foundations for the awarding of projects in areas defined by the Marine Spatial Planning (POEM). However, the implementation of the regulatory framework is far from sufficient.

Experts such as Tomás Romagosa from RWE, and representatives from companies like Ocean Winds and ABEI Energy, in discussions with Energía Estratégica España, have emphasized that the lack of complementary regulations—such as the Coastal Law or the Renewable Energy Economic Regime (REER)—represents a critical obstacle.

The delay in the auction calls, now scheduled for late 2025, has created uncertainty in the planning and execution of projects.

According to Manuel Fernández from Ocean Winds, defining a clear timeline and a comprehensive regulatory framework is crucial not only to meet the national goal of 1-3 GW installed by 2030, but also to maintain competitiveness against neighboring countries.

There are also other challenges, as noted by Ignacio Asúa from Navantia Seanergies: manufacturing capacity and the availability of specialized professionals, as 7,500 additional professionals will be needed by 2030, especially in areas such as naval engineering and project management, to materialize their ambitions.

Despite the regulatory difficulties, companies continue to bet on offshore wind in Spain.

In 2024 alone, developers registered an additional 5,242 MW, consolidating companies like Qair, which leads with 2,738 MW, and developers like Helios (612 MW), Invenergy (552 MW), and Univergy (540 MW).

This effort is visible in flagship projects such as “NORFEU” with 1,080 MW in Catalonia, driven by Qair, and “PINZÓN” from Univergy, with 540 MW in Galicia, which stand out for their focus on floating technologies and their potential to open new technological frontiers.

These add to Spain’s project portfolio, accumulating around 28 GW of capacity.

Among the projects in progress, several stand out for their size and ambition. Capital Energy, one of the leading players in the sector, tops the list with a total capacity of 3,304 MW, distributed across projects like Xistral and others in Galicia.

Grupo Cobra follows with 3,199.6 MW, while ABEI Energy and Qair maintain a solid presence with 2,934.8 MW and 2,738 MW, respectively.

Other key developers include Ferrovial (2,715 MW), IberBlue Wind (2,532 MW), and the BlueFloat Energy and Sener consortium, with 2,440 MW.

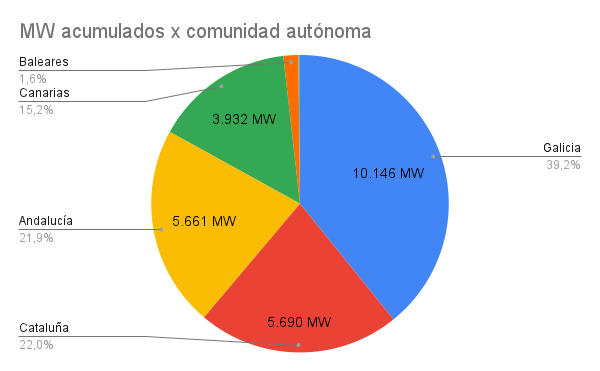

Geographically, Galicia stands out as the leading region, with 10,146 MW in projects under development, representing nearly 40% of the total capacity. Its potential to develop floating offshore wind energy, combined with its port infrastructure, makes it a strategic area.

Catalonia ranks second, with 5,690 MW, driven by notable projects like NORFEU and other initiatives led by Qair. Andalucía follows closely with 5,661 MW, benefiting from its access to the Atlantic and its proximity to key industrial centers.

The Canary Islands also play a crucial role, with 3,932.4 MW. This region has been highlighted by several companies as the ideal location for the first auctions due to its favorable environmental conditions and defined territorial framework. Finally, the Balearic Islands and the Basque Country complete the map with 420 MW and 45 MW, respectively.

2024 Project List

| File Number | Project | Capacity (MW) | Location | Developer | Status | Year |

|---|---|---|---|---|---|---|

| 20240351 | TRAMUNTANA WIND MENORCA | 240 | Balearic Islands | Tramuntana Wind | INITIATED | 2024 |

| 20240316 | MARINE ENERGY RESEARCH PLATFORM OF CATALONIA – PLEMCAT | 30 | Catalonia | IREC | INITIATED | 2024 |

| 20240302 | NORFEU | 1080 | Catalonia | Qair | PREVIOUS CONSULTATIONS | 2024 |

| 20240285 | BREIXO | 648 | Galicia | Qair | PREVIOUS CONSULTATIONS | 2024 |

| 20240222 | PINZÓN | 540 | Galicia | Univergy | PREVIOUS CONSULTATIONS | 2024 |

| 20240190 | ROLEIRA | 594 | Galicia | Qair | PREVIOUS CONSULTATIONS | 2024 |

| 20240187 | TAMARAGUA | 236 | Canary Islands | Qair | PREVIOUS CONSULTATIONS | 2024 |

| 20240153 | WHEEL PROTOTYPE INSTALLATION FOR FLOATING OFFSHORE WIND | 6 | Canary Islands | ESTEYCO | PREVIOUS CONSULTATIONS | 2024 |

| 20240152 | GRANADILLA | 50 | Canary Islands | Capital Energy & BlueFloat Energy | INITIATED | 2024 |

| 20240125 | GREGAL | 180 | Balearic Islands | Qair | PREVIOUS CONSULTATIONS | 2024 |

| 20240116 | MILETO | 612 | Andalusia | Helios | PREVIOUS CONSULTATIONS | 2024 |

| 20240113 | ELAWAN | 240 | Canary Islands | Elawan | PREVIOUS CONSULTATIONS | 2024 |

| 20240099 | O BOI | 552 | Galicia | Invenergy | PREVIOUS CONSULTATIONS | 2024 |

| 20240098 | POSEIDÓN | 234 | Andalusia | Magtel | PREVIOUS CONSULTATIONS | 2024 |

Leading Companies in the Sector

- Capital Energy and Grupo Cobra lead the list of developers, with projects totaling 3,304 MW and 3,199.6 MW, respectively. Both companies have adopted a comprehensive approach, covering everything from environmental permits to prototype development and collaboration with local shipyards.

- ABEI Energy (2,934.8 MW), with a strong presence in Galicia and the Canary Islands, is preparing to capitalize on the planned auctions at the end of 2025.

- Qair (2,738 MW) and Ferrovial (2,715 MW) round out the top 5, solidifying their positions as key players in the transition to a sustainable energy matrix.

- Other companies such as IberBlue Wind, BlueFloat Energy, Iberdrola, and Helios also have significant involvement, with capacities ranging from 612 MW to 2,532 MW.

Canary Islands: Focus for the First Auction

With 3,932.4 MW in projects under processing, the Canary Islands are positioned as a strategic hub for the development of floating offshore wind in Spain. The region will host the country’s first offshore wind auction, attracting a diverse range of developers and key projects.

Key Projects in the Canary Islands:

- Granadilla (50 MW) developed by Capital Energy & BlueFloat Energy.

- Varuna (300 MW) and other projects by ABEI Energy.

- Bandama (195 MW) by Ferrovial.

- Timanfaya (50 MW) by Capital Energy.

- Canawind I and Canawind II (250 MW each) by Grupo Cobra.

2025 Auction: A Landmark for Floating Offshore Wind

The expected 2025 auction will be a crucial milestone for establishing Spain as a leader in floating offshore wind. The publication of Royal Decree 962/2024 in September 2024, which regulates electricity generation from renewable sources in marine installations, established a combined process for access to the grid, maritime space, and tariffs, streamlining and speeding up the project award process.

This advancement is key to maintaining competitiveness against other countries and enabling Spain to meet its renewable energy development goals.