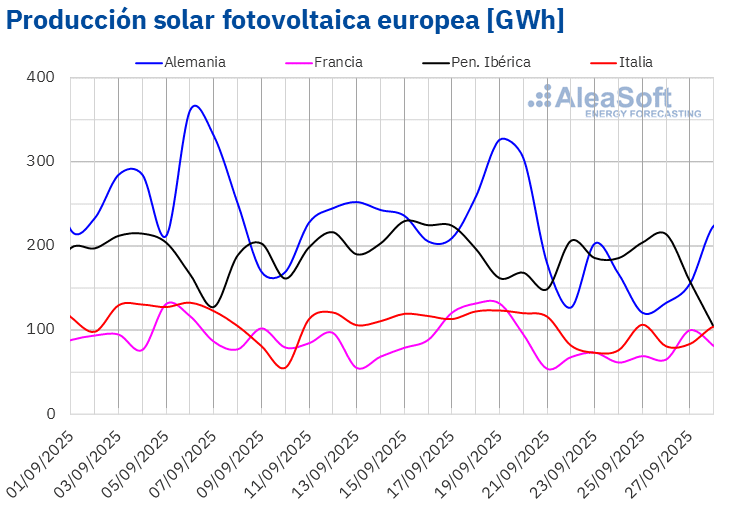

During the week of September 22, solar PV production decreased in the main European electricity markets compared to the previous week, reversing the upward trend of the previous week. The German market experienced the largest drop, 34%. It was followed by the Italian and French markets, with declines of 27% and 26%, respectively. The declines were relatively smaller in the Iberian Peninsula. In the Spanish market, PV generation fell by 7.5% and in the Portuguese market by 4.3%. In the latter case, this downward trend continued for the second consecutive week.

During the week of September 29, according to AleaSoft Energy Forecasting ‘s solar production forecasts , the downward trend will reverse, with an increase in solar photovoltaic production in the Italian and German markets. However, the Spanish market will experience a decline in solar production.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.

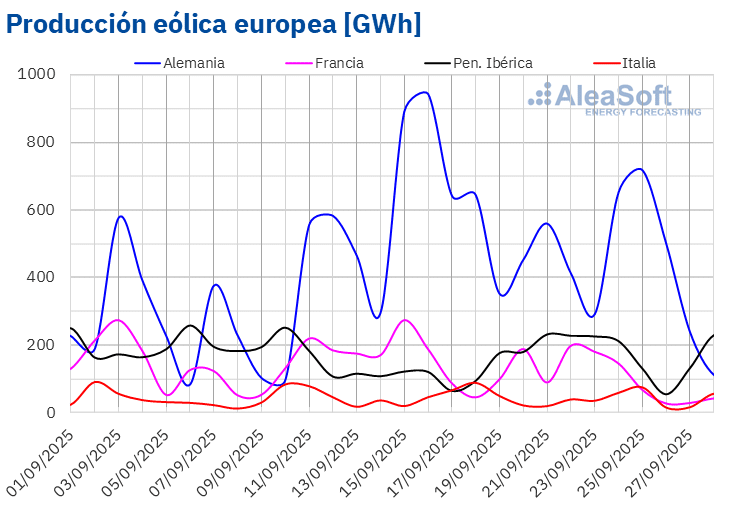

During the fourth week of September, wind energy production increased in the Iberian Peninsula compared to the previous week, marking a reversal of the downward trend recorded at the time. In the Portuguese market, production using this technology increased by 52%, while in the Spanish market it rose by 16%. Furthermore, on September 28, daily wind energy production in the Portuguese market reached 74 GWh, a level last seen at the end of April 2025.

However, in the rest of the major European markets analyzed, wind energy production declined. In the German and French markets, it fell by 35% and 29%, respectively. In the German market, this decline came after three consecutive weeks of increases. The downward trend in the French market continued for a third week. The Italian market recorded the smallest drop, at 4.6%, reversing the upward trend of the previous two weeks.

In the week of September 29, according to AleaSoft Energy Forecasting ‘s wind energy production forecasts , wind energy production will increase in the Italian market and decrease in the German, French, Spanish, and Portuguese markets.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE and TERNA.Electrical demand

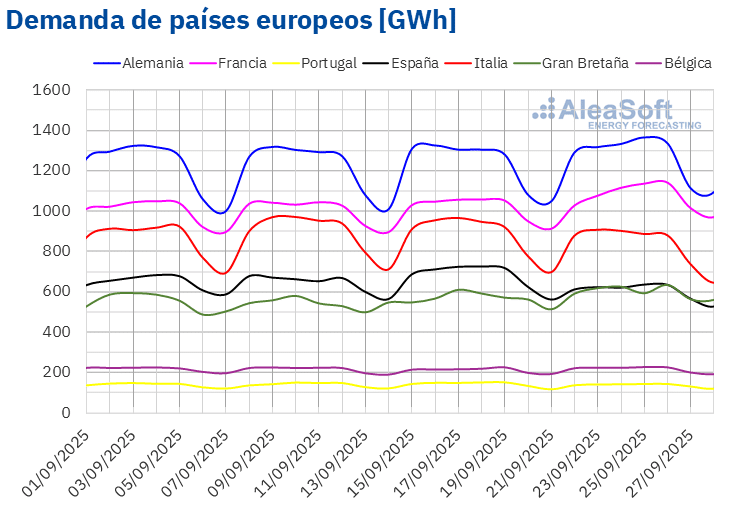

During the week of September 22, electricity demand increased in most of the major European electricity markets compared to the previous week. The British and French markets recorded the largest increases, 5.6% and 5.3% respectively, continuing the upward trend observed the previous week. The Belgian market recorded the smallest increase, 2.2%, reversing the downward trend of the previous two weeks. In contrast, Southern European markets experienced a week-on-week decrease in electricity demand. The Spanish market recorded the largest drop, 11%. The Italian and Portuguese markets saw declines of 5.4% and 3.7%, respectively. In the Italian market, the downward trend continued for the second consecutive week. The Iberian markets reversed the upward trend of the previous week.

During the week, average temperatures decreased in the markets analyzed, with drops ranging from 3.2°C in Italy to 6.4°C in France.

For the week of September 29, according to AleaSoft Energy Forecasting ‘s demand forecasts , demand will decrease in most major European markets, although it is expected to increase in the British market.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting with data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.European electricity markets

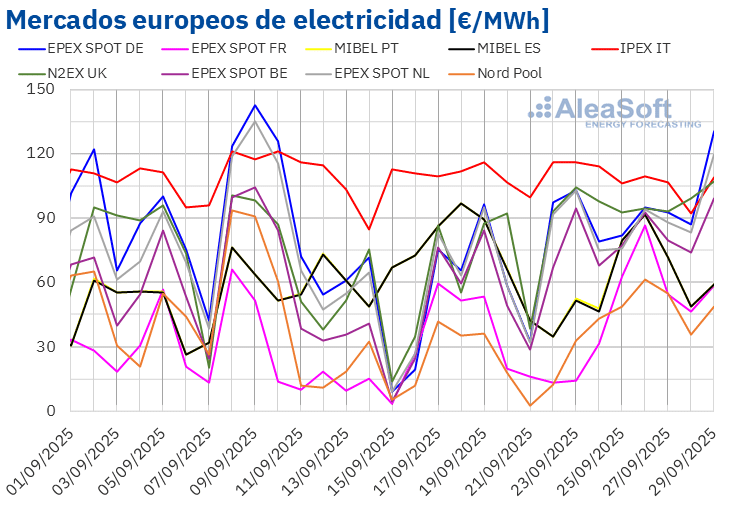

In the fourth week of September, average prices in most major European electricity markets rose compared to the previous week. The exceptions were Italy’s IPEX market , with a slight decrease of 0.9%, and Spain’s and Portugal’s MIBEL market , with a fall of 18%. France’s EPEX SPOT market recorded the lowest price increase, at 34%. In contrast, the Nordic countries’ Nord Pool market achieved the highest percentage price increase, at 92%. In the rest of the markets analyzed by AleaSoft Energy Forecasting , prices rose between 65% in the United Kingdom’s N2EX market and 78% in the German EPEX SPOT market.

During the week of September 22, weekly averages were above €60/MWh in most European electricity markets. The exceptions were the Nordic and French markets, whose averages were €41.27/MWh and €44.17/MWh, respectively. The Italian market recorded the highest weekly average, €108.67/MWh. In the rest of the markets analyzed by AleaSoft Energy Forecasting , prices ranged from €60.59/MWh in the Spanish market to €96.39/MWh in the British market.

Regarding daily prices, on Monday, September 22, the Nordic market reached the lowest weekly average among the markets analyzed, at €12.49/MWh. The French market also recorded daily prices below €15/MWh on September 22 and 23.

Meanwhile, the Italian market continued to record daily prices above €100/MWh for almost the entire fourth week of September. On September 23, this market reached its highest daily average of the week, €116.20/MWh. On that day, the German, British, and Dutch markets also reached daily prices above €100/MWh. On Monday, September 29, daily prices in these four electricity markets were above €100/MWh again. On that day, the German market recorded its highest daily price, €130.57/MWh.

During the week of September 22, the decline in solar and wind production in most markets, as well as the increase in electricity demand in many of them, fueled higher prices in most European electricity markets. However, the increase in wind production and the fall in demand in the Iberian Peninsula contributed to the decline in prices in the MIBEL market.

AleaSoft Energy Forecasting ‘s price forecasts indicate that, in the first week of October, prices will rise in most of the main European electricity markets, influenced by the decline in wind energy production. Furthermore, some markets will register increases in electricity demand, and solar energy production will decline in the Spanish market.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, EPEX SPOT, Nord Pool and GME.Brent, fuels and CO 2

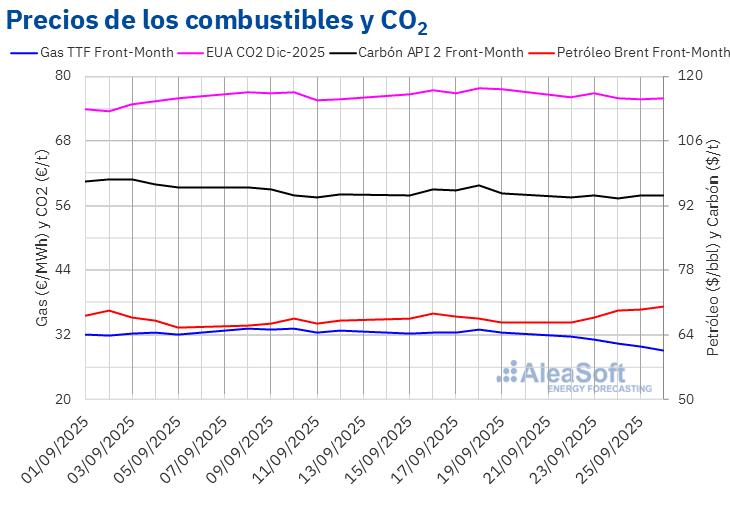

Brent oil futures for the Front-Month on the ICE market registered their weekly minimum settlement price of $66.57/bbl on Monday, September 22. Prices subsequently increased. As a result, on Friday, September 26, these futures reached their weekly maximum settlement price of $70.13/bbl. According to data analyzed by AleaSoft Energy Forecasting , this price was 5.2% higher than the previous Friday and the highest since August 1.

Supply concerns caused by Ukrainian attacks on Russian energy infrastructure, as well as declining US stockpiles, fueled higher Brent crude oil futures prices in the fourth week of September. However, agreements reached to resume oil exports from Kurdistan, as well as expectations of further production increases at the upcoming OPEC+ meeting, could exert a downward influence on prices in the first week of October.

Regarding TTF gas futures on the ICE Front-Month market, on Monday, September 22, they registered their weekly minimum settlement price of €31.84/MWh. Subsequently, prices were higher, but remained below €33/MWh during the fourth week of September. On Friday, September 26, these futures reached their weekly maximum settlement price of €32.70/MWh. According to data analyzed by AleaSoft Energy Forecasting , this price was 1.2% higher than that of the previous Friday.

In the fourth week of September, TTF gas futures prices remained below €33/MWh, driven by abundant supplies of liquefied natural gas. Also contributing to this trend were European stockpile levels, which average over 80% and in some countries are already above 90%.

Regarding CO2 emission rights futures on the EEX market for the December 2025 reference contract, settlement prices remained above €76/t during the first three sessions of the fourth week of September. On Tuesday, September 23, they reached their weekly maximum settlement price of €76.81/t. However, on Thursday, September 25, these futures registered their weekly minimum settlement price of €75.76/t. On Friday, September 26, the price was slightly higher, at €75.97/t. Even so, according to the data analyzed by AleaSoft Energy Forecasting , this price was 2.0% lower than that of the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.